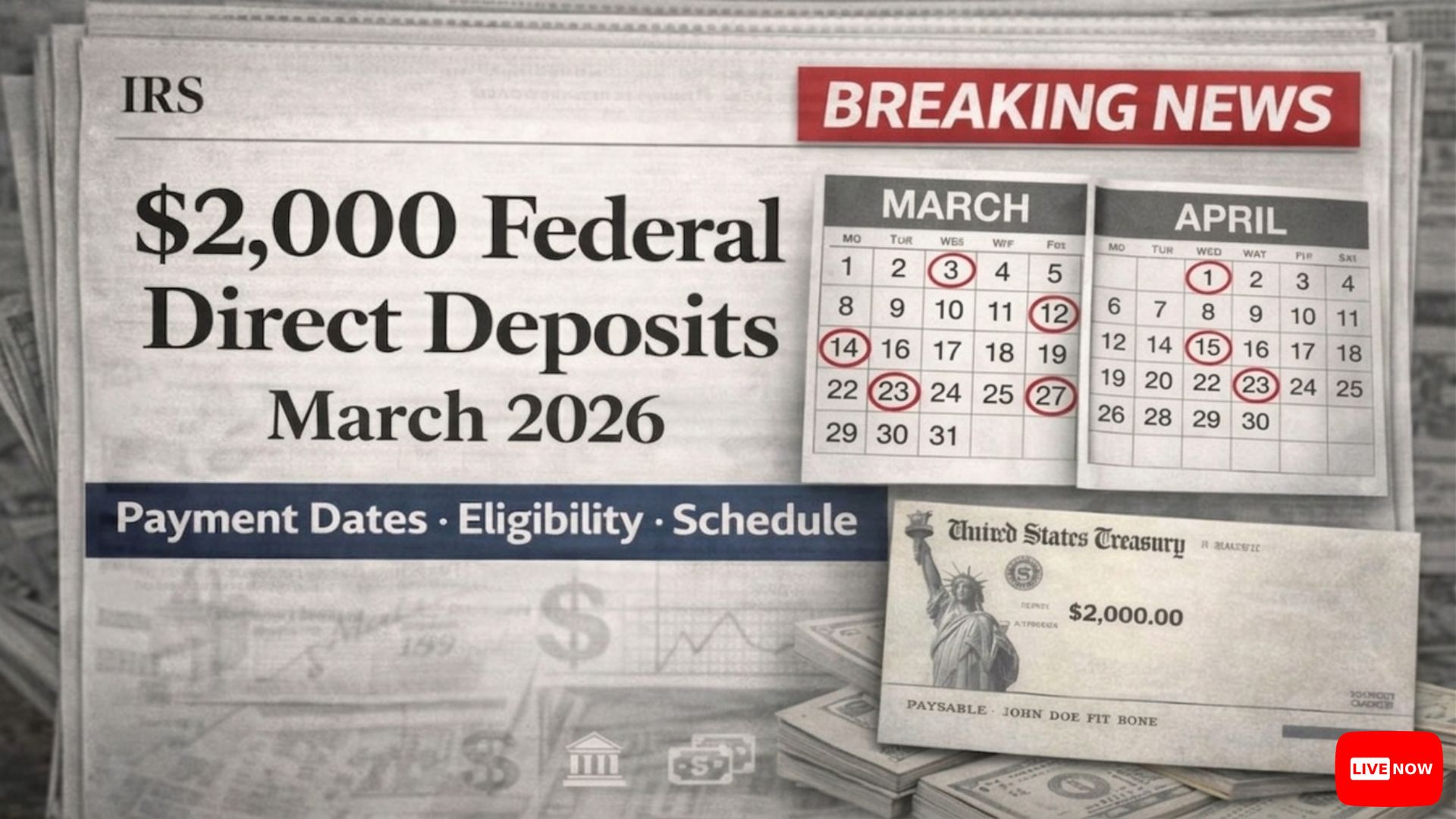

As March 27, 2026, approaches, anticipation is mounting over a proposed $2,000 federal direct deposit that could provide financial relief to many Americans. Rising living costs have heightened the interest in this potential one-time payment, which aims to offer economic support as families navigate ongoing financial pressures. With questions abounding about its authenticity, eligibility criteria, and distribution process, understanding the details of this potential disbursement is crucial.

Understanding the Basis for the March 2026 Payment

The $2,000 payment is envisioned as a one-time federal relief initiative based on legislation enacted in late 2025. It is designed to provide short-term financial stability by supporting individuals and households grappling with persistent cost increases. Importantly, this payment is not a loan or tax refund and does not need to be repaid. Instead, it operates as a direct financial aid measure managed by the IRS using existing tax records.

Distribution Mechanism for Payments

The design of the payment distribution system emphasizes efficiency and speed. The IRS plans to leverage banking details from recent tax returns to facilitate automatic direct deposits into recipients’ accounts. For taxpayers lacking valid direct deposit information, paper checks would be mailed to the address on their most recent tax filing. This streamlined approach seeks to minimize delays and obviate the need for cumbersome application processes or additional registration requirements.

Eligibility Criteria: Income and Filing Status

Eligibility for receiving the $2,000 payment hinges primarily on income levels and filing status, as reported in 2024 federal tax returns. Individuals must meet specific adjusted gross income thresholds: single filers can earn up to $150,000; heads of household can earn up to $225,000; and married couples filing jointly can earn up to $300,000. Additional conditions include having filed a 2024 tax return, possessing a valid Social Security number, and not being claimed as someone else’s dependent.

Timing and Disbursement of Payments

Payments are planned for release in several waves throughout March 2026 rather than as a single nationwide rollout. Direct deposits are expected to appear in bank accounts within a few business days following their release dates. In contrast, paper checks might take several weeks to arrive via mail. It’s important for recipients not to interpret a delay in receiving their payments as an indication of ineligibility; various logistical factors can influence disbursement timing.

Staying Vigilant Against Scams

Given the prominence of government payments like this one, scam attempts often rise alongside official announcements. It is critical for potential recipients to remain vigilant against fraudulent schemes that may try to capitalize on public anticipation and confusion. The IRS will not solicit banking information through phone calls, texts, or emails—any such communication should be treated with extreme caution. Individuals are advised only to trust updates from official government sources.

The proposed $2,000 federal direct deposit stands as a potentially impactful measure aimed at easing economic burdens at the start of 2026. By clarifying eligibility requirements and understanding how payments will be processed and delivered, individuals can better prepare themselves amidst uncertain economic times.

Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Federal payment programs, eligibility rules, and timelines depend on official legislation and government action and are subject to change. Readers should verify details through official IRS communications or consult with a qualified professional before making financial decisions.