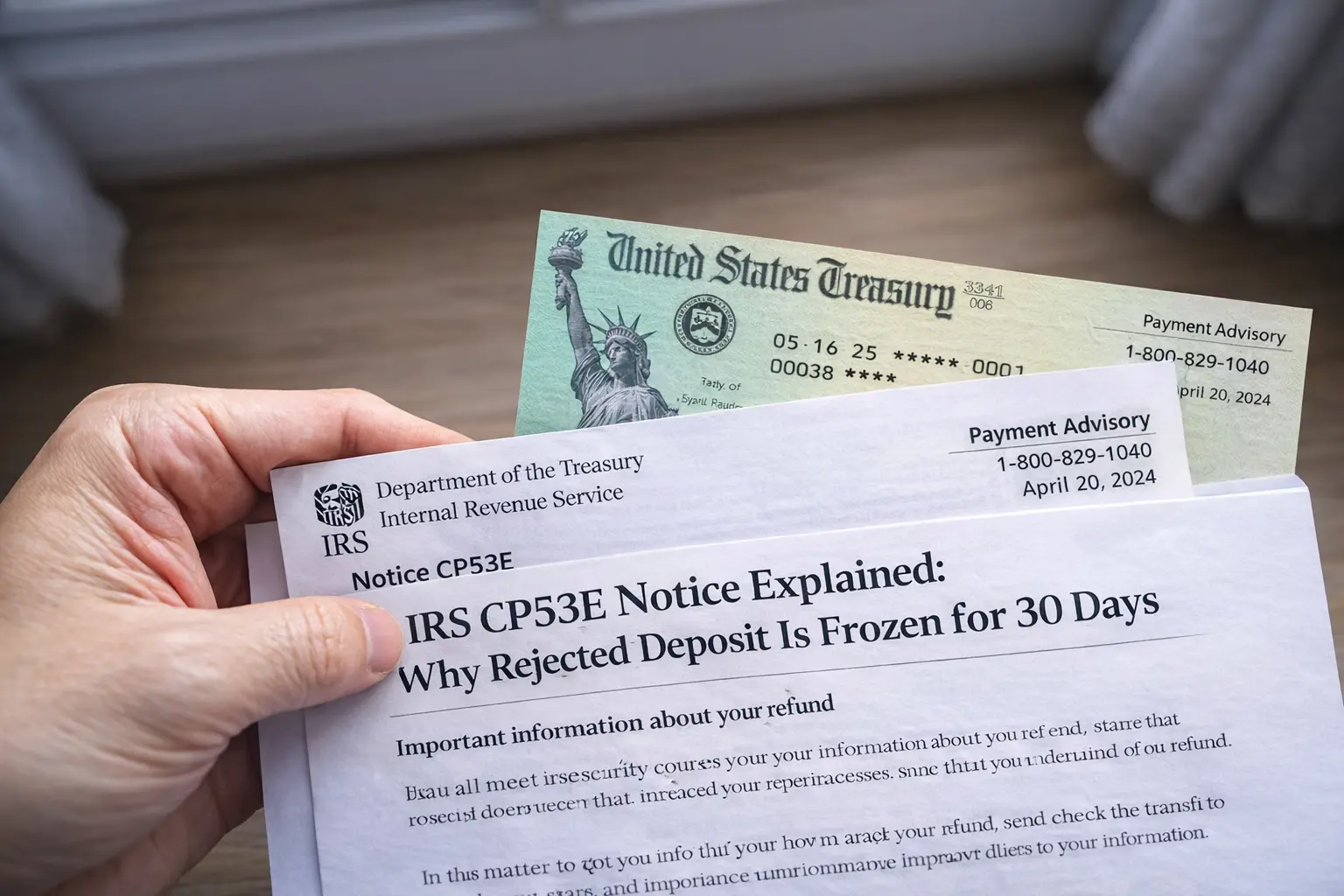

Receiving a CP53E notice from the IRS can be a startling experience, especially when you were eagerly anticipating a tax refund. This notice signifies that your refund has been frozen for 30 days due to a rejected deposit, leaving many taxpayers puzzled and concerned about accessing their hard-earned money. Understanding why this freeze occurs and how to navigate the process of releasing your funds can alleviate stress and ensure your financial plans are not disrupted.

Understanding the CP53E Notice

A CP53E notice is issued by the IRS when an attempted direct deposit of your tax refund is rejected by your bank. This rejection can occur for various reasons, such as incorrect bank account information provided on your tax return or issues related to changes in account status. The notice serves as an official communication informing you of the temporary hold on your refund, which is imposed to ensure that the funds do not end up in an incorrect account. While this may feel inconvenient, it is a protective measure designed to safeguard your finances.

The 30-day freeze period allows both you and the IRS sufficient time to rectify any issues without jeopardizing the security of your refund. During this time, it's crucial to review any recent changes you might have made to your banking details or any other discrepancies that could have led to this situation. Understanding the cause is the first step toward resolving it effectively.

How to Release Your Frozen Refund

Once you've received a CP53E notice, taking prompt action can help in unfreezing your tax refund swiftly. The first step involves verifying the accuracy of the bank account information linked with your tax return. If discrepancies are found, correcting these details with accurate information is essential. This can often be done through online platforms provided by the IRS, such as their official website where you might need to update your financial information.

In some cases, reaching out directly to your bank can clarify whether there have been any recent changes in account status that might have caused the rejection. It's also advisable to keep all correspondence from both the bank and IRS accessible for reference during communications or updates on their online systems.

Communicating with the IRS

Effective communication with the IRS following a CP53E notice is vital in resolving the issue promptly. This involves responding to any requests for additional documentation or clarification that might accompany the notice. The IRS may request verification of identity or confirmation of bank account details as part of their due diligence process.

To expedite matters, utilize electronic communication avenues wherever possible, as they tend to be more efficient than traditional mail during these processes. Ensure that you have all necessary identification documents at hand when engaging in correspondence with the IRS, whether online or via phone, so that they can assist you without unnecessary delays.

Preventing Future Issues

Prevention is better than cure when dealing with potential issues related to tax refunds. To avoid receiving another CP53E notice in future years, take proactive steps during each tax filing season. Double-check all personal and banking information before submitting your tax return to reduce risks of errors leading to rejected deposits.

Consider opting for direct deposit instead of checks whenever possible as this method is generally faster and reduces handling errors. Additionally, keeping detailed records of all banking transactions related to tax refunds will help streamline resolutions should any future discrepancies arise. By staying vigilant about these details annually, you can greatly minimize any disruptions in receiving your expected refunds.

Disclaimer: This article provides general information regarding CP53E notices and does not constitute legal advice or representation. For specific advice regarding individual circumstances or detailed inquiries about a CP53E notice, please consult a tax professional or contact the Internal Revenue Service directly.